Pioneers With Arrows in Their Backs and the Late-Mover Advantage

Pioneers lead the way down the path and end up with arrows in their backs when the next group comes along.

If you have spent any time in the tech world, you’ve probably heard the term “first mover advantage”. Entrepreneurs, business strategists and marketing aficionados like to throw this term around to support their theories of why different companies have a competitive advantage over another.

The phrase “first mover advantage” was first popularized in a 1988 paper by a Stanford Business School professor, David Montgomery, and his co-author, Marvin Lieberman.

This single phrase has become the theoretical underpinning of the out-of-control spending of startups during the dot-com bubble, Silicon Valley and now in the crypto currency industry. Over time the idea that winners in new markets are the ones who have been the first entrants into their categories has become unchallenged conventional wisdom in these tech worlds.

The only problem is that it’s simply not true.

The first-mover advantage is the competitive advantage gained by the initial occupant of a market segment. The first-mover advantage claims to enable a company or firm to establish strong brand recognition, customer loyalty, and early purchase of resources before other competitors enter the market segment.

It is said that the first movers in an industry are almost always followed by competitors that attempt to capitalize on the first movers' success. These followers are also aiming to gain market share in the same industry. It is claimed that most of the time the first-movers will already have an established market share, with a loyal customer base that allows them to maintain their market share.

Many of us have blindly accepted this term into our vernacular and used its theory to build forecasting models with real money at stake. I am as guilty as anyone for using this term, but is there any truth to the theory? Where is the real world evidence to even support its claims?

We’ve Been Duped

Try and think of a company that was a first mover which continues to dominate and lead the industry today by market share. Can you do it? What about some American classics like Coca-Cola? How about Henry Ford and the Ford corporation?

When we rewind history and look back to identify the first movers, we generally make two mistakes: 1. We are unaware of a company's predecessors and their initial attempts to successfully gain adoption, or 2. We misjudge the size of a company and are unaware they have been overtaken by a competitor.

In the case of Coca-Cola and Ford, it’s both. Let’s explore a few examples in dramatically different industries throughout vast time periods.

The Beverage Industry

The Coca-Cola company emerged in 1886, but more than 100 years earlier there were many technologies and companies that paved the way before Coke. In the 1760’s carbonation techniques were first developed. In 1798 the term "soda water" was coined. In 1789 Jacob Schweppe began selling seltzer in Geneva which led to the formation of the Schweppes company which was the first known soda distributor. In 1819 the "soda fountain" was patented by Samuel Fahnestock which led to an explosion of competition in the soda industry. Coca-Cola gained market dominance and became an American classic — nobody thought they could be overtaken, until Pepsi came along. Today, Pepsi has a larger market cap and distribution network than Coca-Cola does. Pepsi dominates the beverage industry with a market cap of 255 billion dollars. Coca-Cola trails by a market cap of only 4.7 billion dollars. Coca-Cola even acquired Schweppes (the first mover) and still trails in comparison.

Automotive Industry

Now let’s dive into the car. Ford Motor Company, founded in 1903, wasn’t the first to manufacture automobiles and Henry Ford didn’t invent the car.

Carl Benz, inventor of the Benz Patent Motorcar in 1885 and founder of the Benz & Cie automotive company is widely regarded as "the father of the car" and "father of the automobile industry", but this is also a misconception. Carl Benz, wasn’t the first. Benz & Cie merged with Daimler Motoren Gesellschaft (Daimler) in 1926 and became Daimler-Benz which produced the Mercedes-Benz. But Daimler wasn’t the first either, which was founded 4 years earlier than Benz in 1890 by Gottlieb Daimler. Daimler and Benz invented cars that looked and worked like the cars we use today. However, it is unfair to say that either man invented the automobile.

Let me introduce you to Sir Goldsworthy Gurney. During the years between 1825–1829 Gurney designed and built a number of steam-powered road vehicles which were intended to commercialize a steam road transport business—the Gurney Steam Carriage Company. His vehicles were built at his Regent's Park Manufactory works. Gurney improved upon the design to the point where he was able to sell vehicles to Charles Dance. Sir Charles Dance was an English pioneer of motoring. An enthusiastic motorist, he did a great deal to encourage engineers who were engaged in the invention and development of steam road vehicles. Dance ran Gurney's coaches on the road between Cheltenham and Gloucester until public opposition compelled his withdrawal.

It’s now clear that Henry Ford, The Ford Motor Company and the famous Model T were not the first movers in the automotive industry, nor was the United States the first country to pioneer automobiles.

Fast forward to 2005– Ford was overtaken by Chevrolet. Today, Ford has a market cap of $55 billion, which is dwarfed by Toyota which comes in at $200 billion. We now have a new contender in the auto market: Tesla, which has a market capitalization of over $600 billion.

Social Media

The saga of social media is a great example of an industry where incumbents are repeatedly subverted by new technologies and companies innovating upon the previous rendition. When we think of social media our minds immediately turn to Facebook, Instagram, Twitter and TikTok—- but before today’s leaders came on the scene there were decades of previous contenders that paved the way.

Social networking goes back to the early days of computers in 1973. Talkomatic was created by 17-year old student Dave Woolley and Douglas Brown at the University of Illinois, as a multi-user chat room application. TERM-Talk was then created by the staff at the Computer-based Education Research Laboratory at the University of Illinois, as an instant-messaging application enabling any two users on the PLATO system to conduct a live, character-by-character typed conversation. PLATO Notes was created by the same Dave Woolley who created Talkomatic as a conferencing and bulletin board forum system for communicating with the user community.

In 1980 the Bulletin Board System (BBS) emerged as one of the earliest known forms of social media. In 1988 Internet Relay Chat IRC rose from the roots of BBS and was initially intended to extend it, offering a similar service and experience.

In 1996 ICQ was released by Israeli company Mirabilis. The name ICQ derives from the English phrase "I Seek You". In 1997 AOL Instant Messenger was released. In 1998 ICQ was acquired by AOL, and the service was patented.

Early social networking on the Internet began in the form of generalized online communities such as Theglobe.com (1995), Geocities (1994) and Tripod.com (1995). These early communities focused on bringing people together to interact with each other through chat rooms and encouraged users to share personal information and ideas via personal web pages by providing easy-to-use publishing tools. Classmates.com took a different approach by simply having people link to each other via email addresses. PlanetAll started in 1996.

In the late 1990s, user profiles were the central feature of social networking sites, allowing users to compile lists of "friends" and search for other users with similar interests. New social networking methods were developed by the end of the 1990s, and many sites began to develop more advanced features for users to find and manage friends. Open Diary, a community for online diarists, invented both friends-only content and the reader comment, two features of social networks important to user interaction.

The newer generation of social networking sites began with the emergence of SixDegrees in 1997. Open Diary in 1998, Mixi in 1999, Makeoutclub in 2000, Cyworld in 2001, Hub Culture in 2002, and Friendster and Nexopia in 2003. Cyworld also became one of the first companies to profit from the sale of virtual goods. MySpace and LinkedIn were launched in 2003 and Bebo launched in 2005. Orkut became the first popular social networking service in Brazil (although most of its very first users were from the United States) and quickly grew in popularity in India. In 2005 MySpace had more pageviews than Google.com.

Twitter launched in 2006 and has since become among the top social networking apps in the United States with close to 400 million users.

In April 2012, the image-based social media network Pinterest had become the third largest social network in the United States.

All of these services were subverted by Facebook which was launched in 2005 and became the largest social networking site in the world by 2009. Meta, which owns Facebook, Messenger and Instagram has a total of 3.7 billion users.

As you can see, social media has had a long journey from its beginnings in 1973. The giants we are all familiar with today have risen out of a highly competitive landscape, all of which were not first movers in the industry. Where are the first movers today? All those pioneers are long dead with arrows in their backs.

First Movers

Over decades and across industries, we see pioneers and first movers repeatedly being overtaken by newcomers. You can see the cycle repeating over and over again:

Local video stores were overtaken by Blockbuster, then by Netflix and other streaming services. Remember TiVo? Every cable company overtook them with DVRs.

Remember MP3 players before the iPod?

PDAs (personal digital assistants), the first one in existence, was pioneered by Apple computers and it was called Newton, it failed and that’s when Palm Pilot took over— now every cell phone is a PDA and Palm Pilots are dead.

Before the iPhone, Blackberry was the smartphone industry leader— nobody thought Apple could compete, especially because it didn't have a physical keyboard.

The Atari Game console was the first of its kind, now the industry is ruled by Sony PlayStation and Microsoft’s Xbox.

The Pebble Smart Watch was overtaken by Apple, Samsung and Fitbit.

Before Spotify we had Rhapsody. YouTube could be the next leader.

Before Microsoft’s Excel we used Lotus 123.

Remember Craigslist? Now everyone uses Facebook Marketplace.

What about Vine? Now it’s TikTok, Facebook Reels and YouTube Shorts.

Before Gmail was launched everyone had a yahoo or hotmail account. Before Gmail, it was AOL.

Where did you buy books before Amazon rose to power? Barnes & Noble managed to hang on, but whatever happened to Borders Books?

What was your favorite search engine before Google came onto the scene? Was it Yahoo? Alta Vista? Lycos? Ask Jeeves?

The first web browser was called WorldWideWeb and later renamed Nexus. Many others were soon developed, with Marc Andreessen's 1993 Mosaic later renamed as Netscape. Those are all now relics of the past. Today, the major web browsers are Chrome, Safari, Internet Explorer, Firefox, Opera, and Edge. And we shouldn’t forget the rising Brave browser with native privacy and crypto features.

We can go on and on with this list, and I’m sure you can think of many in other industries throughout history. We seldom see, if any, examples of an industry first mover that’s still in the lead to this day. The lesson we can learn from this pattern is that no leader stays in its position forever — the longer a first mover has been in the lead, the closer we are to its position being overtaken by a potential competitor — assuming history stays true to its patterns.

Competitors never stop coming after the top dog. Narratives change, culture changes, technology advances, political landscapes shift, dictators rise and fall, new generations are born, older generations die, and history happens.

But why is this phenomenon so? Why has this pattern continued to manifest itself throughout history?

The Handicap of A Head Start

In 1937 a Dutch journalist and historian by the name of Jan Romein published an essay series entitled “The Unfinished Past”. Romein was the first to notice this phenomenon and coined the term “The Handicap of a Head Start” in the essay “The Dialectics of Progress”. His theory suggested that an initial head start in a given area may result in a handicap in the long term.

The law suggests that making progress in a particular area often creates circumstances in which stimuli are lacking to strive for further progress. This results in the individual or group that started out ahead eventually being overtaken by others. In the terminology of the law, the head start, initially an advantage, subsequently becomes a handicap.

Romein states that this phenomenon occurs when a society dedicates itself to certain standards, and those standards change, it is harder for it to adapt. Conversely, a society that has not committed itself yet will not have this problem. Thus, a society that at one point has a head start over other societies, may, at a later time, be stuck with obsolete technology or ideas that get in the way of further progress. One consequence of this is that what is considered to be the state of the art in a certain field can be seen as "jumping" from place to place, as each leader soon becomes a victim of the handicap.

In common terms, societies, companies, and individuals are often confronted with the decision to either invest now and get a fast return, or put off the investment until a new technology has emerged and possibly then make a bigger profit.

Late Movers

Secondary or late-movers to an industry or market have the opportunity to study first-movers and their techniques and strategies. Late movers may be able to 'free-ride' on a pioneering firm's investments in a number of areas including R&D, buyer education and infrastructure development.

The basic principle of this effect is that the competition is allowed to benefit and not incur the costs which the first-mover has to sustain. These imitation costs are much lower than the innovation costs the first-mover had to incur, and can also cut into the profits the pioneering firm would otherwise enjoy.

Late movers are sometimes able to assess a market need that will cause an initial product to be seen as inferior. This can occur when the first-mover does not adapt or see the change in customer needs, or when a competitor develops a better, more efficient, and sometimes less-expensive product. Often this new technology is introduced while the older technology is still growing, and the new technology may not be seen as an immediate threat.

The Flippening

Now, let’s apply these new theories and historical trends to the world of cryptocurrency and blockchains.

In one of my precious articles, Catch the Tsunami of Capital Flowing Into Crypto With Cryptex, I wrote: “If you look back over the past 5 years at the coins that were in the top 10 and 20 rankings of the market, it looks very different than it does today. I think it’s safe to say the next 5 will see a similar shift. Some will survive, some will fail, and some will flip others in the rankings. It’s an endless battle of the king of the hill”.

Let’s explore this in more depth to see how things have really changed.

If you head on over to CoinMarketCap.com there is a fun tool you can play around with to see what I’m talking about. Their “Cryptocurrency Historical Data Snapshot” tool allows you to select any week going back as far as 2013 and see what the rankings of the top cryptocurrencies were. Try it out and you will immediately see that the statement I made in my article is spot on.

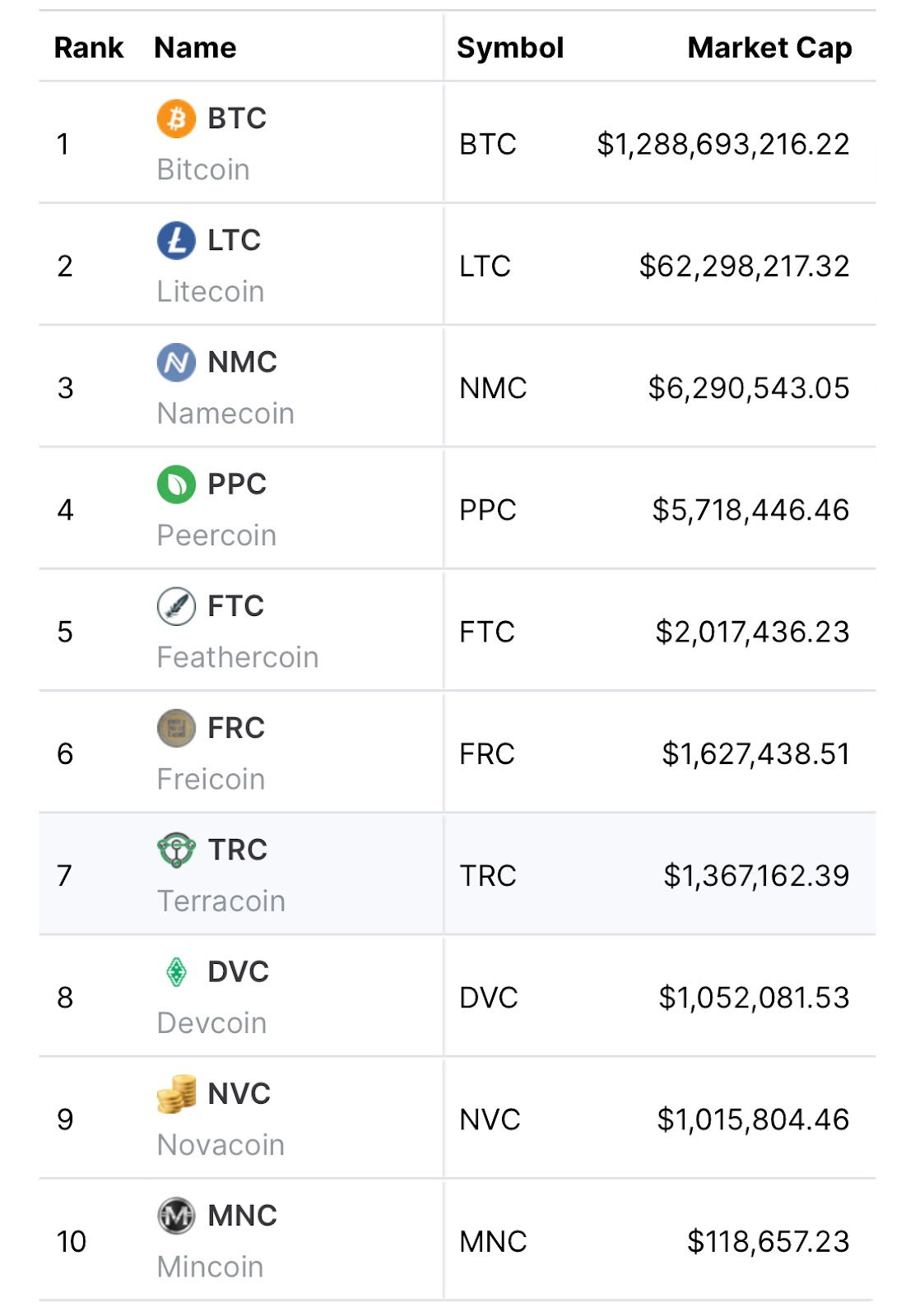

On the week of May 5, 2013, these were the top 10 coins:

You can see Bitcoin in the number 1 rank, Litecoin is number 2, Namecoin 3, Peercoin 4, Feathercoin 5, Freicoin 6, Terracoin 7, Devcoin 8, Novacoin 9 and Mincoin at number 10.

It’s important to note that in 2013, Ethereum wasn’t even invented yet. This would come 2 years later.

Let’s fast forward the clock and see how these projects are doing today. Bitcoin is still in the number 1 position, Litecoin is now in 13th position, Namecoin has dropped to 600th, Peercoin dropped to 700th, Feathercoin is in 1,375th, Freicoin is 2026th, Terracoin is 1,670th, Devcoin no longer exists, Novacoin is in 2,073rd position and finally Mincoin, which does not exist.

There is a popular belief that is circulating among many crypto investors which suggests a strategy of simply buying the top ten cryptocurrencies with the rationale that they are too big to fail and are the most recognized in the industry. We can now use this historical tool to see that cryptos are constantly “flipping” one another in market cap.

“The flippening” is a term used to describe a “flip” in one crypto over another. For years there has been speculation about the possibility of the now second-largest cryptocurrency, Ethereum, overtaking Bitcoin.

Ethereum launched in 2015 and within weeks it quickly rose to the number 4 position. Just 6 months later in 2016 it claimed the number 2 position. Ethereum has been closing the gap hot on the heels of Bitcoin’s lead. Ethereum is outpacing Bitcoin despite Bitcoin’s almost 8 year head start.

Bitcoin was the first mover and it was the only cryptocurrency in existence for the first 2 years of its life. Then, contenders came as we have seen. Bitcoin’s dominance was 100% and over the last 13 years it’s dominance has fallen by over 60%. At the time of writing this, Bitcoin’s dominance represents 39% of the total cryptocurrency market cap.

Are we beginning to see the initial signs of this industry first mover losing its lead?

Catching The Second Wave

In the world of investments, especially crypto, we often hear stories of Bitcoin and Ethereum OG’s brag about how long they have been in the industry and what price they initially purchased their coins at. They are looked upon with envy and it generally leads to an overpowering sense of FOMO (fear of missing out). We think we have missed the boat on an investment opportunity of a lifetime. But have we?

Bitcoin and Ethereum are categorized as “Layer 1” protocols. A Layer 1 protocol is the basic network of a blockchain network or ecosystem. All transactions done on the network are executed by Layer 1 and its native token is used for the transaction fees.

I believe we are in the initial stages of a market takeover by a new cast of layer 1 projects throwing their hat in the ring.

If we revisit our current cryptocurrency leaderboard we will see a fascinating trend emerging. Six out of the top 10 cryptos are Layer 1 projects. If we expand our view, we can see that 12 out of the top 20 are Layer 1s. It’s clear that the competition for layer 1 protocols is fierce and many are competing for market dominance. But this competition isn’t new. And some of these high ranking projects have been at it for over a decade — 2011 in the case of Litecoin and 2012 with Ripple. Projects like Cardano and TRON have been working on their layer 1 solutions for almost 5 years now.

But there is a new cast of characters that have recently emerged in this competitive landscape. Solana and Avalanche were launched in 2020 and both quickly rose to the top 20 Solana and Avalanche are testaments to the strong appetite of the market for new layer 1 solutions. This appetite comes from the notion that the first movers in the industry have had anywhere from 5 years to over a decade to fulfill their promises and demonstrate the performance of their products. New entrants to the market have new technologies, new theories and fresh eyes on the ecosystem.

We are starting to see the side effects that come with being the first movers to an industry. The initial head start that some of these projects had are starting to result in a handicap. The stimuli that has caused these projects to strive for further progress is weakening. They have had years to deliver, unlimited capital, the attention of the entire industry and top talent all working towards their success.

The conditions are ripe for new contenders to emerge and overtake the incumbents. Solana and Avalanche are strong candidates and they will most likely do well in the coming years, but I want to introduce you to a new layer 1 project that could be among the top industry performers.

My area of expertise is finding trends and getting interested in things well in advance of those things becoming interesting to lots of other people. This naturally coincides with the market cap of a particular investment being small, or smaller relative to others in an industry.

Let’s return to our crypto leaderboard and scroll down to number 35. This is where we will find our next contender: NEAR Protocol.

NEAR Protocol

NEAR is the next generation of blockchains and it will enable Web3 to reach the masses. NEAR is a Layer 1 blockchain and it uses a unique scaling mechanism which makes it especially easy to onboard new users through named accounts. It opens the door to mass adoption for Web3.

Usability and speed have been the biggest hurdles that crypto is trying to overcome. Most users of crypto, if you want to call them that, simply use centralized exchanges to hold their coins for speculative purposes — much like Robinhood for stocks. If users want to take the next step into the land of Web3 and cryptocurrency, they must go deeper down the rabbit hole which includes great complexity and risk. Users must become the custodians of their crypto by holding and securing their own cryptographic keys and use an entire stack of applications which inter operate with each other to perform the desired function. There have been great efforts made to educate new users and many have made it across the divide, but the vast majority of users we will need for mass adoption will not cross over until the tools are in place to do so. In Web3, your money is at stake— any errors can lead to lost or stolen funds.

Near Protocol is setting out to solve these problems. NEAR is a simple, scalable, and secure blockchain platform designed to provide the best possible experience for developers and users, which is necessary to bridge the gap to mainstream adoption of decentralized applications.

Unlike other blockchains, NEAR has been built from the ground up to be the easiest in the world for both developers and their end-users while still providing the scalability necessary to serve those users. Their mission is to onboard users with a smooth experience, even if they have never used crypto, tokens, keys, wallets, or other blockchain tools. The underlying platform automatically expands capacity via sharding without additional costs or effort on your part.

NEAR has an impressive core team and notable venture capital backing. Alexander Skidanov, one of the founders of NEAR previously worked for Microsoft and Illia Polosukhin (founder) worked for Google. This year, 2022, NEAR closed a $500 million dollar funding round which has given them the means to support and further the development of the protocol and growth of the ecosystem. This creates a perfect environment for growth especially in the current bear market condition we are experiencing. NEAR has already amassed over 22 million user accounts and conducts more than 400 thousand transactions per day- Their transaction speeds are down to only 2.4 seconds, an impressive achievement which beats many of the existing layer 1 incumbents.

NEAR even has a low energy footprint and is certified carbon neutral by South Pole, the industry lead in carbon offsetting solutions. NEAR's innovative blockchain design uses a fraction of the energy other networks use, and requires no sort of power-draining "crypto mining" to perform transactions.

The venture capital backing behind NEAR is also extremely impressive with some notable supporters such as a16z and Coinbase Ventures. NEAR currently has a market cap of 1.4 billion and a token price of $1.71. The NEAR token can be purchased on most major exchanges including Coinbase.

Adam Grant, the author of Originals wrote in his book that 47% of first mover companies, or pioneers, would fail in their early years compared to only 8% of so-called improvers or settlers. If you are afraid you have missed the layer 1 blockchain, DeFi or Web3 movements, you haven’t. With the crypto bear market in full effect, now is the time to support the projects quietly building their new technologies that will overtake yesterday’s market leaders.